Are banks focusing on the right metrics for sustainable cost improvements?

Cost management in the banking industry often falls into focusing solely on cost-cutting. However, for cost improvements to be successful, they should be sustainable. This requires a continuous review of spending, optimizing current resources, driving efficiencies, and shifting savings to investments that deliver value to the bank and its customers.

This is the cost transformation mindset. And it requires additional metrics for gauging success.

Explore our survey data and get the latest insights on cost optimization in banking in this new report by KPMG International.

KPMG International’s initial analysis of survey results from global banks, indicates a consistent decrease in banks cost-to-income ratio (CIR) pre-COVID, followed by an increase during FY19-21 likely due to staff, technology costs, and loan loss provisioning. Recently, improvements in CIR have been observed, largely due to top-line gain from rising interest rates that have boosted profitability.

However, with rising inflation, cost management has become more crucial for banks. Services and people costs tend to increase in line with inflation, and the risk of reduced income is becoming a reality in many countries due to the cost of living/borrowing crisis.

While CIR and return on equity (ROE) are widely used to gauge bank performance, a deeper focus is needed to measure performance more broadly.

By considering customer metrics such as the cost-to-serve (CTS) and full-time equivalents (FTE) per customer, banks can focus on productivity, efficiency, and profitability. Implementing new technologies, simplifying processes, and introducing efficiency initiatives can increase customer value.

Adopting a cost-culture mindset

In the KPMG Banking cost transformation survey, 82 percent of respondents identified deep cultural challenges in achieving sustainable cost reductions, despite significant technology investments. Most banks aim to reduce costs, but their cost-reduction objectives often do not align with their broader ambitions, and a cost-culture mindset is not embedded throughout the organization.

Cost transformation in banks does not always permeate the entire organization, even when executives are compensated for meeting cost objectives. Some banks have implemented horizontal and vertical cost structures to align business needs with spending. Executives responsible for a vertical, such as retail banking, are also responsible for its associated costs.

Get ready for the next wave of cost transformation

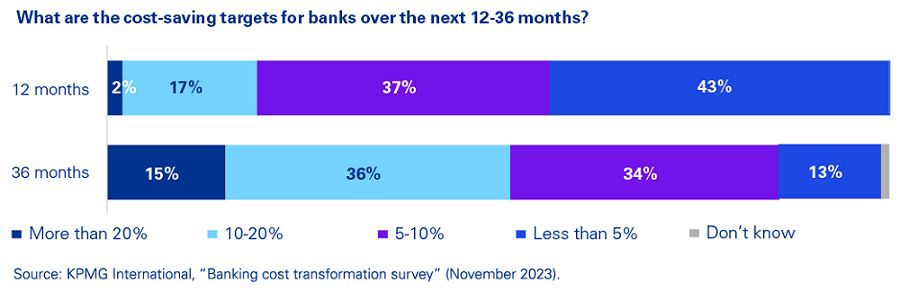

The KPMG Banking cost transformation survey showed that despite recent improvements in CIR, there is a clear need to deliver additional value — and at a greater pace — in the next wave of cost transformation investments. Research suggests that this will be in the region of 10 percent in cost efficiencies over the next 12 months and as high as 20-30 percent over the next three years. Set against an inflationary headwind, these will be significant targets to achieve.

Based on the foundational work that many banks have already put in place, leaders are more confident about where the costs sit. Eighty-six percent of bank executives feel they have strong cost-base mapping in place, with three out of four believing they have the right incentives in place for leaders to achieve their targets.

In KPMG professionals’ experience working with bank executives, many examples point to the impact of these executives’ investments on the operating expenses of contact centers and branches that shift to digital channels, the front-to-back digitization of core value streams such as personal lending and mortgages, and the consolidation of functions to drive scale. However, unanticipated headwinds, changes in customer demands and the challenges of stopping to do certain things means that all too often the gains made are reversed as other costs are added.

As banks look at the next wave of cost transformation investments, the themes are consistent as the strategy begins to extend beyond traditional frontline functions into the FTE base in corporate-headquartered departments and functions such as Finance, Risk and Compliance and Marketing.

How KPMG can help

KPMG has developed a 12-lever model that sits alongside Value Analysis/Value Engineering thinking and provides banks with an opportunity to consider their options for increasing value and reducing the cost to serve. With most banks endeavoring to drive value with one or more of the levers, it continues to maintain its relevance.

The broad learnings gained from KPMG professionals’ experience with banks and other financial services organizations leads to three steps for banks to consider in developing their cost transformation strategies and assessing, funding and executing the supporting business cases.

- Value and cost are the primary objectives. In some banks, there is more investment in contact centers or relationship managers to drive differentiated service and increase market share. When tied with AI supported co-pilots, this can be a powerful resource for banks to invest in.

- Design the cultural mechanisms that will have the biggest impact for your organization. For some, this can be top-down cost boards and cost management units tied to zero-based budgeting concepts. For others, more value may be achieved through a Hoshin Kanri-style concept to fully align your organization around the highest-impact investments.

- Measure the real costs that exist across entire value chains and the options you have to deploy the 12 levers in a way that will move the value equation in the right direction vs. just cutting costs, leaving the functional elements underdeveloped and finding that costs begin to creep back into the business over time.

KPMG firms have an international team of cost transformation professionals who have worked with the world’s leading global, regional and local banks. We can help assess potential earnings improvements, define functional cost-saving strategies and develop an execution plan tailored to your organization.

About the report

In November 2023, KPMG International conducted a survey with over 200 banking leaders, supported by extensive benchmarking and 1-1 interviews with leaders who are developing the next wave of strategic cost and value optimization investments.

Why work with KPMG in Thailand

KPMG in Thailand, with more than 2,000 professionals offering Audit and Assurance, Legal, Tax, and Advisory services, is a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee.